Futures: Overnight, LME copper opened at $9,833/mt, rose to a high of $9,872/mt, and fell to a low of $9,808/mt, closing at $9,846.5/mt. The overall trend showed initial downward fluctuations followed by a rebound. The decline was 0.61%, with a trading volume of 26,000 lots and open interest of 311,000 lots. Overnight, the most-traded SHFE copper 2505 contract opened at 80,930 yuan/mt, rose to a high of 81,160 yuan/mt, and fell to a low of 80,550 yuan/mt, closing at 80,810 yuan/mt. The overall trend was downward. The decline was 0.93%, with a trading volume of 84,000 lots and open interest of 223,000 lots.

[SMM Copper Morning Meeting Summary] News: (1) After the recently announced auto tariffs may trigger retaliatory actions from the EU and Canada, US President Trump warned these two major US allies of imposing higher tariffs. Trump threatened that if the EU and Canada jointly harm the US economy, the US will impose hefty tariffs. Trump posted on social media that the tariffs would "far exceed current plans."

(2) Against the backdrop of increasing uncertainty, China has clarified a moderately loose monetary policy. The central bank has repeatedly cut the RRR and interest rates to support economic development through monetary policy adjustments. The policy stance is clear: China will cut the RRR and interest rates as appropriate based on domestic and overseas economic and financial conditions.

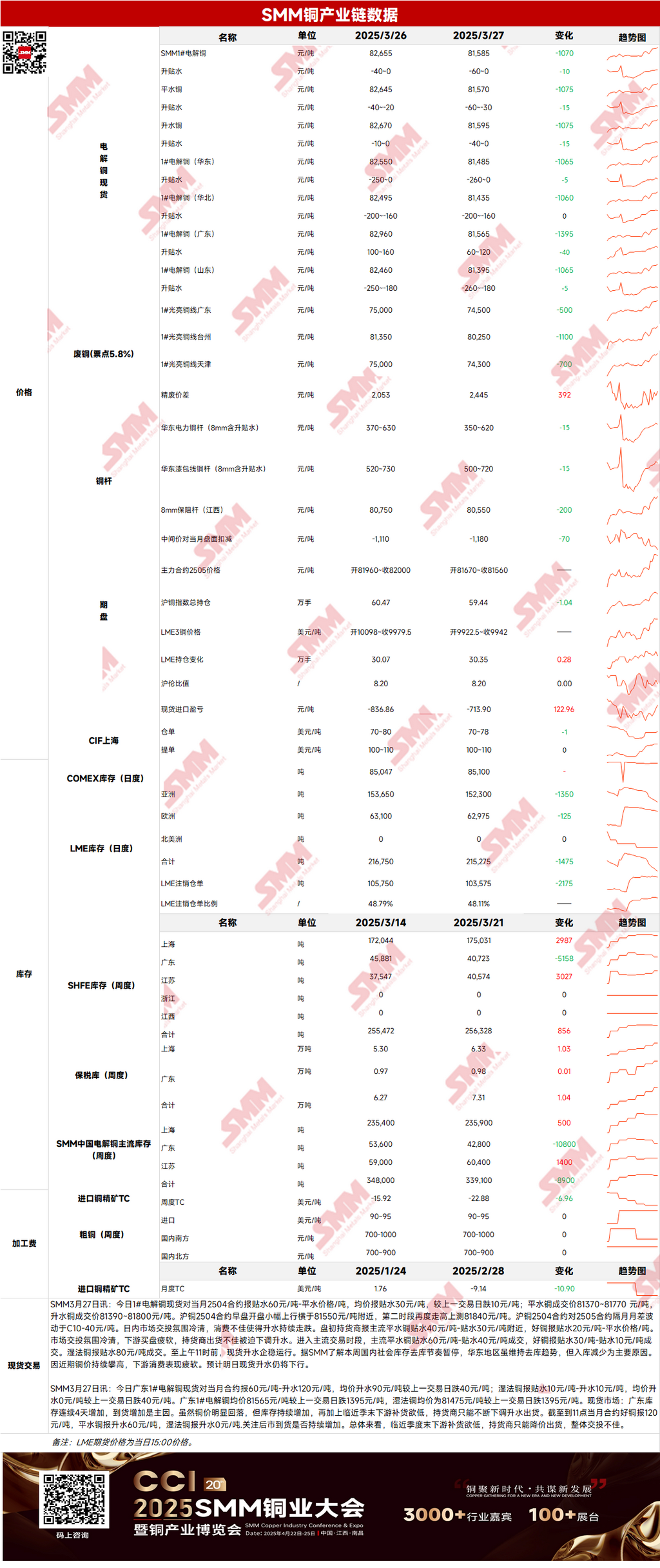

Spot: (1) Shanghai: On March 27, spot prices of #1 copper cathode against the front-month 2504 contract were at a discount of 60 yuan/mt to parity, with an average discount of 30 yuan/mt, down 10 yuan/mt MoM. According to SMM, the destocking pace of domestic social inventory paused this week. Although east China maintained a destocking trend, the main reason was reduced inflows. Due to the recent continuous rise in copper prices, downstream consumption has been weak. Spot premiums are expected to continue to decline today.

(2) Guangdong: On March 27, spot prices of #1 copper cathode in Guangdong against the front-month contract were at a discount of 60 yuan/mt to a premium of 120 yuan/mt, with an average premium of 90 yuan/mt, down 40 yuan/mt MoM. Overall, as the quarter-end approaches, downstream restocking demand is low, and suppliers can only lower prices to sell, resulting in poor overall trading.

(3) Imported copper: On March 27, warrant prices were $70-78/mt, QP April, with an average price down $1/mt MoM; B/L prices were $100-110/mt, QP April, with an average price flat MoM. EQ copper (CIF B/L) was $40-50/mt, QP April, with an average price flat MoM, referencing shipments arriving in early to mid-April. Overall, market transactions were limited, and actual prices showed a pullback trend.

(4) Secondary copper: On March 27, secondary copper raw material prices fell by 500 yuan/mt MoM. Bare bright copper prices in Guangdong were 74,400-75,600 yuan/mt, down 500 yuan/mt from the previous day. The price difference between copper cathode and copper scrap was 2,445 yuan/mt, up 392 yuan/mt MoM. The price difference between copper cathode rod and secondary copper rod was 1,665 yuan/mt. According to SMM, due to severe weather, Ningbo Port was temporarily shut down for 36 hours. Local import traders reported that due to fog and heavy rain, arriving ships could not unload normally or were delayed, but the severe weather is not expected to last long, and the port is expected to return to normal the day after tomorrow.

(5) Inventory: On March 27, LME copper inventories decreased by 1,475 mt to 215,275 mt; on March 27, SHFE warrant inventories decreased by 1,662 mt to 137,906 mt.

Price: Macro-wise, Thursday's US data showed a decline in initial jobless claims last week, but the market reacted little. The US dollar was mixed on Thursday as the market speculated on how severe the tariff measures announced by US President Trump next week might be, with uncertainty still disturbing the market. On the supply side, the destocking pace of domestic social inventory paused this week. Although east China maintained destocking, it was mainly due to reduced inflows. As of Thursday, March 27, SMM's mainstream copper inventory in China slightly increased to 334,500 mt, marking the fourth consecutive week of weekly destocking. Next week, both imported copper arrivals and domestic copper increments will be limited, and total supply will remain low. On the demand side, due to the recent high copper prices, downstream consumption has been weak, and market trading has been sluggish, with spot premiums falling. Prices are expected to continue to decline tomorrow. Price-wise, with no macro positives and limited fundamental support, if domestic spot transactions remain sluggish today, copper prices may continue to fall.

Click to view the SMM Metal Database

[The above information is based on market collection and comprehensive evaluation by the SMM research team. The information provided in this article is for reference only. This article does not constitute direct advice for investment research decisions. Clients should make decisions cautiously and not use this as a substitute for independent judgment. Any decisions made by clients are unrelated to SMM.]